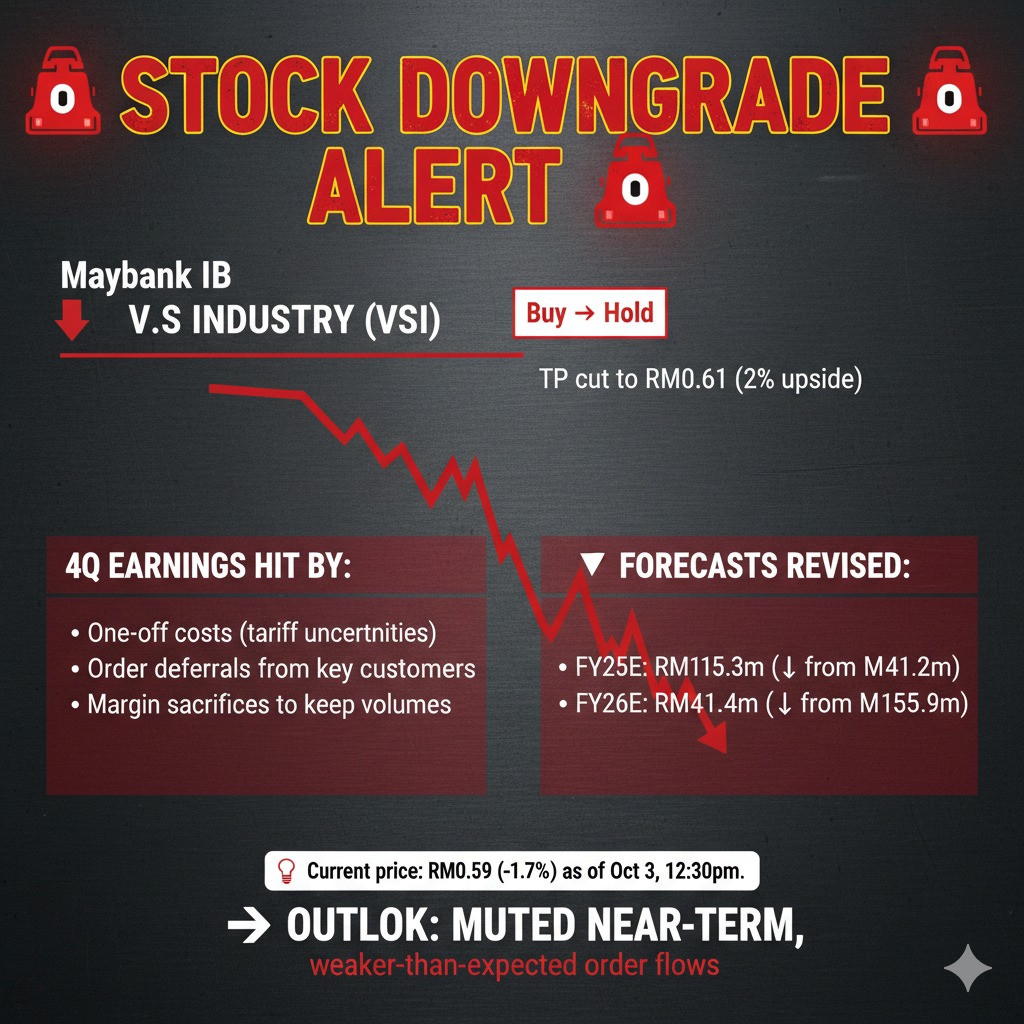

V.S Industry Bhd (VSI) has come under renewed pressure following its latest earnings briefing. Maybank Investment Bank has downgraded the stock from Buy to Hold and slashed its target price to RM0.61 (from RM0.71), implying a meagre 2% upside from current levels.

Weak 4Q Earnings on Margin Compromise

The EMS (electronics manufacturing services) player saw its 4Q earnings fall short as one-off costs were incurred due to tariff uncertaintiesand order deferrals from key customers. To maintain business volumes, VSI accepted less favourable terms—effectively sacrificing margins to sustain operations.

This compromise, however, weighed heavily on profitability, signalling that the company’s near-term outlook is not as robust as previously expected.

Forecasts Cut on Slower Orders

Reflecting this weaker environment, Maybank IB has trimmed its earnings forecasts by 9–18%. The revisions were made to account for softer order inflows amid ongoing tariff uncertainties and customer hesitancy.

- FY25E core earnings lowered to RM115.3m (from RM141.2m)

- FY26E core earnings revised to RM141.4m (from RM155.9m)

The cuts highlight the challenges VSI faces in sustaining growth without margin concessions, especially given its reliance on major customers.

Analyst Track Record

Notably, the covering analyst—who mainly tracks the Industrial Products & Services sector—has an average return of -10% with a 26% success rate on calls over a 3-month horizon. This data point may temper confidence in the downgrade, though the fundamentals underpinning the revised view remain clear.

Market Reaction

As of 12:30 p.m. on October 3, VSI’s share price slipped 1.7% to RM0.59, trading just below the newly revised target price. This reflects investors’ cautious stance following the earnings miss and weaker-than-expected guidance.

Outlook

With profitability pressured by margin compromises and uncertainty clouding customer demand, VSI’s near-term prospects look muted. While the company remains a key EMS player in the region, investors may need to brace for a slower recovery unless order momentum picks up and tariff clarity emerges.

Leave A Comment